Handheld Ultrasound Market Size, Portable Diagnostic Imaging Trends and Forecast 2026–2034

- Ajit Kumar

- Apr 3

- 4 min read

Handheld Ultrasound Market Overview Analysis By Fortune Business Insights

Market Size & Forecast

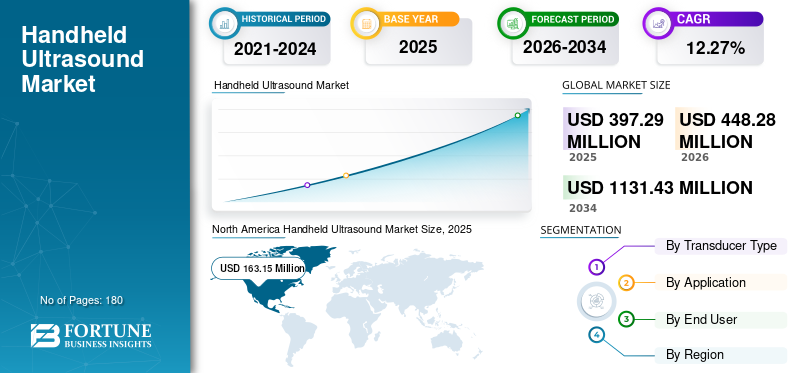

According to Fortune Business Insights: The global handheld ultrasound market was valued at USD 397.29 million in 2025 and is projected to grow from USD 448.28 million in 2026 to USD 1,131.43 million by 2034, recording a robust CAGR of 12.27% over the forecast period. North America led the market in 2025, accounting for a 41.07% share of global revenue.

What Is Handheld Ultrasound?

Handheld ultrasound refers to compact, portable imaging devices that connect to mobile platforms or standalone ultrasound systems, enabling rapid, bedside diagnostic decisions by healthcare providers. Unlike traditional bulky ultrasound machines, these devices offer unmatched portability and ease of use, making them increasingly valuable in emergency care, point-of-care settings, home healthcare, and remote or resource-limited environments. Their growing adoption reflects a broader shift in healthcare toward decentralized, real-time diagnostics.

Get a Sample Research PDF: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/100702

Key Market Drivers

Rising Prevalence of Chronic and Acute Conditions The expanding global burden of cardiovascular disease, cancer, urological disorders, and other chronic conditions is a primary force propelling demand for handheld ultrasound devices. As diagnostic rates rise alongside growing patient populations, the need for fast, accessible imaging tools intensifies. According to the World Health Organization, there were an estimated 20 million new cancer cases globally in 2022, underscoring the scale of diagnostic demand. The rapidly aging global population amplifies this further — the U.S. Population Reference Bureau projects that Americans aged 65 and above will rise from 58 million in 2022 to approximately 82 million by 2050.

Increasing Per Capita Healthcare Expenditure Rising healthcare spending, particularly in developed markets, is enabling broader investment in advanced diagnostic technologies. The U.S. per capita healthcare expenditure stood at USD 14,570 in 2023, facilitating sustained adoption of premium point-of-care devices. Adequate reimbursement frameworks and supportive regulatory policies in North America and Europe further reinforce market expansion.

Key Market Trends

AI and Technology Integration The most transformative trend reshaping the handheld ultrasound landscape is the integration of artificial intelligence and machine learning into imaging platforms. AI-powered systems offer automated measurements, real-time image interpretation, and enhanced detection accuracy for conditions such as tumors and musculoskeletal injuries. In April 2024, GE Healthcare launched its CaptionAI software on the Vscan Air SL system to enable rapid AI-driven cardiac assessments, exemplifying the sector's momentum toward intelligent, automated diagnostics.

Point-of-Care and Home Healthcare Adoption Demand for point-of-care ultrasound (POCUS) is accelerating in emergency and critical care units, driven by the devices' speed and portability. Simultaneously, adoption in home healthcare settings and medical education institutions is growing, prompting manufacturers to develop more user-friendly, wireless solutions tailored to non-traditional clinical environments.

Market Restraints & Challenges

The principal restraint facing the market is the high cost of advanced handheld devices, which limits adoption in price-sensitive emerging markets. Device prices can reach several thousand dollars, creating affordability barriers, especially where refurbished equipment markets offer lower-cost alternatives.

Regulatory complexity presents a further challenge. Compliance requirements imposed by agencies such as the U.S. FDA and the European Union are rigorous and time-consuming, increasing the cost and time-to-market for manufacturers. Limited reimbursement coverage in certain geographies adds another layer of constraint. Additionally, handheld devices still lag behind premium stationary systems in capabilities such as 3D/4D imaging, advanced Doppler functions, and deep tissue penetration, which may limit their appeal for specialized clinical use cases.

Segmentation Analysis

By Transducer Type: The phased array segment led the market in 2024, favored for its compact footprint, strong tissue penetration, and sector-shaped image output — qualities particularly valuable in cardiac imaging. The linear segment is expanding steadily, driven by growing demand for high-resolution superficial imaging applications.

By Application: Radiology dominated in 2024, supported by the rising volume of ultrasound examinations in dedicated imaging departments and the expanding number of radiology centers globally. The cardiology segment is expected to grow at a strong pace, fueled by the high global incidence of heart disease — the CDC reports approximately 805,000 heart attacks annually in the U.S. alone.

By End User: Hospitals represented the largest end-user segment, reflecting their high patient throughput and advanced diagnostic infrastructure. Diagnostic imaging centers are also growing rapidly, driven by the benefits of early disease detection and cost-effective outpatient care models.

Regional Outlook

North America leads globally with USD 163.15 million in 2025 (41.07% share), supported by high healthcare spending, robust reimbursement policies, and a concentration of leading manufacturers driving continuous product innovation.

Asia Pacific is the fastest-growing region, contributing 32.15% of global revenue in 2025 (USD 127.74 million), with strong momentum expected through 2034. Improving healthcare infrastructure in China, India, and Southeast Asia, combined with a massive and underserved patient base, makes the region a key growth engine. China alone reports approximately 330 million individuals affected by cardiovascular disease.

Europe accounted for 23.46% of the global market in 2025 (USD 93.21 million), growing at a steady CAGR driven by an aging population, rising awareness of early diagnosis, and active governmental promotion of ultrasound-based screening programs.

Latin America and Middle East & Africa represent smaller but developing markets, with expanding hospital networks and growing diagnostic center infrastructure gradually building adoption capacity.

Connect with Our Expert for any Queries: https://www.fortunebusinessinsights.com/enquiry/speak-to-analyst/100702

Competitive Landscape & Key Developments

The market is semi-consolidated, with GE Healthcare, Koninklijke Philips N.V., and Butterfly Network, Inc. holding significant shares. Other active players include Shenzhen Mindray, Clarius, CHISON Medical Technologies, Konica Minolta, and SuperSonic Imagine. Recent milestones include SuperSonic Imagine's December 2024 launch of the PocketVu handheld diagnostic system, Clarius receiving FDA approval for an AI-driven fetal biometric measurement tool in June 2024, and Exo Imaging securing FDA clearance for AI tools on its Iris handheld system in April 2024.

Conclusion

The global handheld ultrasound market is on a high-growth trajectory, underpinned by the convergence of rising chronic disease prevalence, technological advancement, and expanding healthcare access worldwide. As AI integration deepens and emerging markets mature, handheld ultrasound is positioned to redefine the boundaries of accessible, real-time diagnostic imaging across clinical and non-clinical settings alike.

Comments