UAV Propulsion System Market Size, Drone Powertrain Innovations and Growth Forecast 2026–2034

- Ajit Kumar

- 6 days ago

- 3 min read

UAV Propulsion System Market Overview By Fortune Business Insights

Market Snapshot

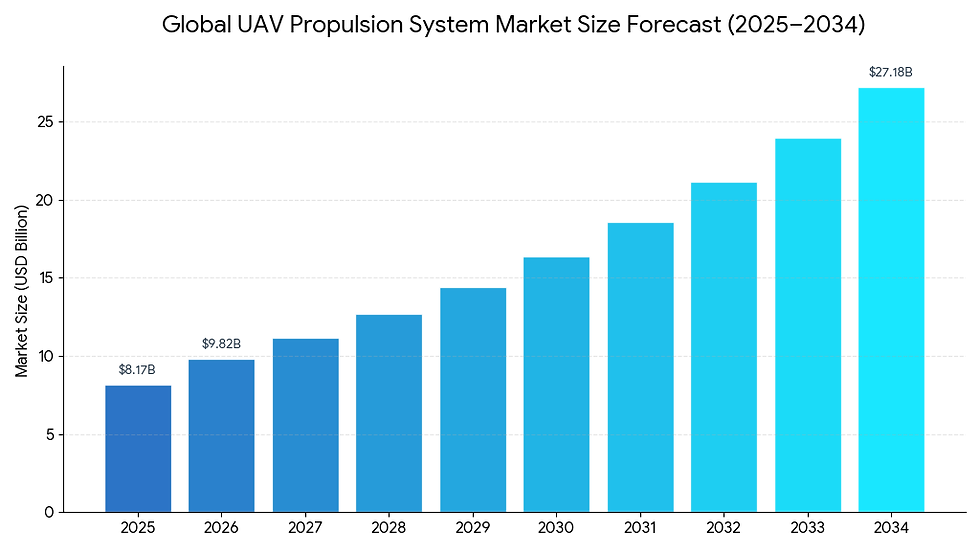

According to Fortune Business Insights: The global UAV propulsion system market was valued at USD 8.17 billion in 2025 and is projected to grow from USD 9.82 billion in 2026 to USD 27.18 billion by 2034, at a compound annual growth rate (CAGR) of 13.6%. North America led the global market with a 31.33% share in 2025.

The market encompasses all hardware required for drones to fly — engines, electric motors, propulsors, energy sources, and control electronics. Rising demand is being driven by longer flight time requirements, heavier payload capacities, extended range missions, and rapid adoption of Beyond Visual Line of Sight (BVLOS) operations across both defense and commercial sectors.

Get a Sample Research PDF: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/115343

Key Market Drivers

Mass procurement of attritable drones and loitering munitions is the primary growth driver. Militaries are purchasing drones at industrial scale — systems that get deployed, lost, and replaced rapidly. This transforms propulsion into a high-volume business, increasing demand for motors, engines, batteries, and spare parts. In January 2025, AeroVironment received a USD 55.3 million delivery order for Switchblade loitering munitions under a U.S. Army contract with a ceiling value of up to USD 990 million.

BVLOS regulatory reforms represent a significant near-term opportunity. When approvals become easier to obtain, drone programs can scale from pilots to full commercial deployments in inspection, mapping, logistics, and public safety — all of which demand higher-endurance propulsion technologies, including hybrid systems and hydrogen fuel cells.

Key Market Restraints & Challenges

Export controls and cross-border supply chain complexities are constraining growth. Stricter regulations resulting from geopolitical tensions — including the Russia-Ukraine conflict and U.S. tariffs — have complicated global access to engines, motors, power electronics, and raw materials such as aerospace alloys and battery minerals.

Critical raw material risk is another significant challenge. Electric propulsion systems depend on lithium, nickel, cobalt, graphite, and rare-earth magnets. Supply constraints drive up costs, particularly for high-power electronics and long-endurance battery packs. The EU's Critical Raw Materials Act (Regulation (EU) 2024/1252), in effect since May 2024, addresses this by establishing frameworks to secure access for strategic sectors including defense and aerospace.

Segmentation Highlights

By Propulsion Type: Battery-electric systems dominated in 2025, owing to their simplicity, low maintenance, and compatibility with multirotors and short-range VTOL platforms. Hybrid-electric is the fastest-growing sub-segment, projected at a CAGR of 17.0%.

By UAV Platform: Multirotors led the market due to their suitability for commercial operations — quick deployment, precise hovering, and low operating costs. VTOL/Hybrid VTOL is the fastest-growing platform segment at a CAGR of 18.3%.

By UAV Class: Small UAVs dominated, offering an optimal balance of cost, capability, and scalability across both commercial and tactical applications. Loitering munitions are the fastest-growing class at a CAGR of 17.1%.

By Fuel Type: Li-ion batteries held the largest share, as they are lightweight, energy-dense, and sufficient for most multirotor and small UAV applications. Hydrogen and solar-based alternatives represent the fastest-growing fuel category at a CAGR of 16.7%.

By Component: Energy storage and fuel systems led all components, reflecting the premium placed on endurance and reliability. Power electronics and control is the second-fastest-growing component segment at a CAGR of 14.2%.

By End User: Defense dominated due to massive government investment in ISR and combat capabilities. The civil/commercial segment is the fastest-growing at a CAGR of 14.3%.

Regional Outlook

North America holds the largest market share, underpinned by substantial U.S. defense spending, a strong aerospace manufacturing base, and favorable FAA policies supporting commercial drone adoption. The U.S. market alone was valued at approximately USD 2.41 billion in 2025.

Europe is growing at a CAGR of 14.0%, driven by the Russia-Ukraine war's impact on defense demand and European efforts to reduce reliance on external suppliers. Germany and France are the region's two largest contributors.

Asia Pacific is the fastest-growing region at a CAGR of 16.1%, fueled by large-scale defense modernization and a broad commercial drone base. China leads the region with revenues of USD 1.05 billion in 2025; India accounts for approximately 16% of regional revenues.

Middle East is the second-fastest-growing region at a CAGR of 15.9%, with Turkey, Israel, the UAE, and Saudi Arabia as key markets tied to defense and border surveillance applications.

Connect with Our Expert for any Queries: https://www.fortunebusinessinsights.com/enquiry/speak-to-analyst/115343

Competitive Landscape

The market is shaped by three key competitive pillars: supply chain resilience, access to repair and sustainment services, and energy system performance. Leading players include Honeywell International, Rolls-Royce, Safran Group, GE Aerospace, Pratt & Whitney (RTX), and specialists such as Hirth Engines, Sky Power GmbH, ZeroAvia, and T-Motor. Industrial-scale manufacturing partnerships are increasingly influencing market share, as consistent delivery, cost efficiency, and production quality now matter as much as raw performance.

Comments